What’s Principal® Intelligent QDIA?

A modern approach to provide participants greater investment personalization and flexibility.

Principal® Intelligent QDIA is a hybrid qualified default investment alternative (QDIA) that can help meet the rising demands from both plan sponsors and participants for a more flexible and personalized default.1, 2

What’s a hybrid QDIA?

A hybrid QDIA (also known as dynamic QDIA or dynamic default) is an innovative way to modernize the plan’s default investment to help meet the needs of a diverse workforce.

A hybrid QDIA uses two complementary default investment alternatives to evolve with participants as their retirement savings needs can change—automatically transitioning them to a more personalized default option when their financial needs may be more complex.

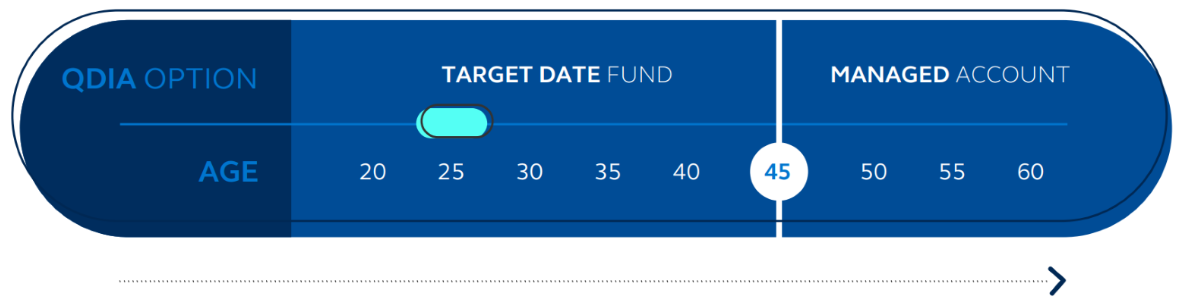

How Principal® Intelligent QDIA works

Principal® Intelligent QDIA is a hybrid QDIA that allows the plan sponsor to choose two QDIA options and the age at which participants automatically transition from one default to the next—our suggestion is age 45.

Principal® Intelligent QDIA example:3

- One QDIA—such as a target date fund (TDF) or RetireView®—for defaulted participants up to age 45 to help build their retirement savings when they may have less complicated financial needs.4

- A second QDIA—a managed account service—for participants age 45+ that can provide more personalized advice (with additional participant input) as their financial situation may become more complex and they begin to think about retirement.

For illustrative purposes only.

Four reasons plan sponsors may consider a hybrid QDIA

Participants say they want and need more help, and that includes wanting advice in the plan’s default investment.2

- Employees #1 stressor is not saving enough for retirement5

- Most participants look to the plan’s QDIA to make investment decisions6

- Participants want the plan to use a hybrid QDIA that gets more personalized with age2

- Nearly one-third say they support the plan automatically nudging them to personalized advice closer to retirement2

Most plan sponsors anticipate a dynamic QDIA with a target date fund and managed account service to be the most common plan default by 2030.7

Benefits of Principal® Intelligent QDIA

Principal® Intelligent QDIA eliminates the need for plan sponsors to weigh the pros and cons of selecting one default investment for all participants. It allows plan sponsors the flexibility to use a complementary approach that could be considered the best of both.

Using a hybrid QDIA to help drive potential outcomes

Potential for plan sponsors: Each retirement plan will have different characteristics, but some plan sponsors may choose a hybrid QDIA to:

- Help drive plan results with a comprehensive QDIA that seeks to improve participants’ retirement outcomes

- Modernize the plan’s QDIA with a next generation offering that’s built on the foundation of the Pension Protection Act (PPA)

- Nudge participants to holistic confidence-boosting advice that can help answer some of their biggest retirement savings questions8

- Provide potential for a more tailored asset allocation strategy for later-stage and pre-retiree workers

Potential for participants: Using a hybrid QDIA to nudge participants to advice when they may need it most may help:

- Boost confidence8

- Increase savings9, 10

- Improve investment returns9

- Achieve their retirement income goals10

Flexible asset allocation choices

Supporting plan sponsors with asset allocation options we make available, Principal® Intelligent QDIA can deliver the choice and flexibility needed to help meet participants’ varying levels of financial complexity and help prepare them to reach their retirement goals.

Learn more

To get started, contact your local Principal® representative or support team:

Call us at 800-952-3343

Email our Advisor Support Team

About target date investment options:

Target date portfolios are managed toward a particular target date, or the approximate date the investor is expected to start withdrawing money from the portfolio. As each target date portfolio approaches its target date, the investment mix becomes more conservative by increasing exposure to generally more conservative investments and reducing exposure to typically more aggressive investments. Neither the principal nor the underlying assets of target date portfolios are guaranteed at any time, including the target date. Investment risk remains at all times. Asset allocation and diversification do not ensure a profit or protect against a loss. Be sure to see the relevant prospectus or offering document for full discussion of a target date investment option including determination of when the portfolio achieves its most conservative allocation.

1 Managed accounts as QDIA increased from 5% in 2020 to 9% in 2021 and hybrid QDIA increased from 3% in 2020 to 5% in 2021, U.S. Retirement Markets 2021, Cerulli and Associates, December 2021.

2 58% of participants have an interest in managed accounts. 32% of participants want their plan to use a hybrid QDIA and 30% want their employer to automatically move them to personalized advice later in their career. Principal® Retirement Security Survey – Investments, July 2022.

3 With either option, investing involves risk, including possible loss of principal.

4 The participant will be defaulted into the applicable target date fund in the series based on the plan’s normal retirement date.

5 U.S. Retirement End-investor 2022 – Fostering Comprehensive Relationships, The Cerulli Report, 2022.

6 58% defaulted in QDIA and more look to it to make an elective decision. Principal data, Jan. 1, 2022, through June 30, 2022.

7 86% of plan sponsors and 76% of financial professionals agree the most common default option by 2030 will likely be a target date with a managed account service. Principal® Future of Retirement Survey, January 2023.

8 Confidence in choosing investments increases from 35% without to 65% with advice. Confidence in investment performance boosts 914%, going from 7% without to 71% with advice. Confidence in ability to achieve retirement goals increases 838%, going from 8% without to 75% confident with advice. Principal® Retirement Security Survey – Investments, July 2022.

9 Managed accounts: A personalized employee benefit for retirement and financial wellbeing. Alight, April 2022.

10 Plan sponsors who offer managed accounts say the top reason is that it helps drive retirement outcomes. U.S. Retirement Markets 2021, Cerulli and Associates, December 2021.

Important information

The subject matter in this communication is educational only and provided with the understanding that Principal® is not rendering legal, accounting, investment, or tax advice. You should consult with appropriate counsel, financial professionals, and other advisors on all matters pertaining to legal, tax, investment, or accounting obligations and requirements.

Investing involves risk, including possible loss of principal.

Asset allocation and diversification does not ensure a profit or protect against a loss. Equity investment options involve greater risk, including heightened volatility, than fixed-income investment options. Fixed-income investments are subject to interest rate risk; as interest rates rise their value will decline. International and global investing involves greater risks such as currency fluctuations, political/social instability, and differing accounting standards. These risks are magnified in emerging markets. Fixed-income and asset allocation investment options that invest in mortgage securities are subject to increased risk due to real estate exposure. The performance and risks of a fund of funds directly correspond to the performance and risks of the underlying funds in which the fund invests.

There is no guarantee that a target date investment will provide adequate income at or through retirement. A target date fund’s (TDF) glide path is typically set to align with a retirement age of 65, which may be your plan’s normal retirement date (NRD). If your plan’s NRD/age is different, the plan may default you to a TDF based on the plan’s NRD/Age. Participants may choose a TDF that does not match the plan’s intended retirement date but instead aligns more to their investment risk. Compare the different TDF’s to see how the mix of investments shift based on the TDF glide path.

Investment advice is provided by an SEC-registered investment advisor (RIA) and delivered through a managed account service. Advice is based on the information provided about you and is limited to the investment options available in the defined contribution plan. Projections and other information regarding the likelihood of various retirement income and/or investment outcomes are hypothetical in nature, do not reflect actual results, and are not guarantees of future results. Results may vary with each use and over time. All investments involve risk, including the loss of principal. There can be no assurance that any financial strategy will be successful.

Past performance does not guarantee future results. The RIA does not guarantee that the results of their methodologies or the objectives of a strategy will be achieved.

Assumptions involve known and unknown risks, uncertainties, and other factors which may cause actual results to differ materially and/or substantially from any expected future result, performance, or achievement expressed or implied by those assumptions for any reason.

Asset allocation and diversification are investment methodologies that do not ensure a profit or protect against a loss in a declining market.

RetireView® is an educational service designed to help retirement plan participants determine an appropriate investment mix for their retirement account. Principal retained Morningstar Investment Management LLC, a registered investment adviser and a subsidiary of Morningstar, Inc., to create asset class-level model portfolios (“Models”) for RetireView. In no way should Morningstar Investment Management’s creation of the Models be viewed as advice or establishing any kind of advisory relationship with Morningstar Investment Management. Morningstar Investment Management does not endorse and/or recommend any specific financial product that may be used in conjunction with the Models. Morningstar Investment Management LLC is not an affiliate of any company of the Principal Financial Group®. See additional important information here.

Principal charges each participant who enrolls or defaulted in the managed account service a fee for the RIA. In addition to this fee, assets invested through the Managed Account service are also subject to fees and expenses of the underlying investment options and recordkeeping services. Insurance products and plan administrative services are provided through Principal Life Insurance Company®. Securities offered through Principal Securities, Inc., member SIPC and/or independent broker-dealers. Referenced companies are members of the Principal Financial Group®, Des Moines, Iowa 50392.

Principal®, Principal Financial Group®, and Principal and the logomark design are registered trademarks of Principal Financial Services, Inc., a Principal Financial Group company, in the United States, and are trademarks and services marks of Principal Financial Services, Inc., in various countries around the world.

Intended for financial professional use.

© 2023 Principal Financial Services, Inc. | 2867701-062023 | 06/2023